NPS or New Pension Scheme is a retirement product launched by Government of India. It is managed by PFRDA (Pension Fund Regulatory and Development Authority). This product helps you to create retirement corpus. NPS was launched on 1st Jan 2004 initially it was for the central Govt Employees (Except Armed Forces ).Later NPS was made available for ll the citizens of the country with effect from 1st May 2009

Eligibility

Any citizen of India (whether resident or NRI) can invest in this scheme. The age of the subscriber must be within 18-60 years of age. However, an individual of unsound mind or existing members of NPS are not allowed to open new account. Therefore, an individual can open only ONE NPS account.

When you Open NPS Account you have to choose the following

1. Pension fund Manager

2. Type of NPS Account

3. Investment Choices

lets understand all the above in Detail

Pension Fund managers:

1. HDFC Pension Fund management Co. Ltd.

2. ICICI Prudential Pension Fund Management Co.Ltd.

3. Kotak Mahindra Pension Fund Management Co.Ltd

4. LIC Pension Fund Ltd.

5. SBI Pension Fund Pvt Ltd

6. UTI Retirement Solutions Ltd.p

7. Aditya Birla Sun Life Pension Management Ltd

Note: You can change the fund Manager

NPS Account:

1. Tier 1 Account : This is a Retirement Account Subscribers can withdraw from this account only upon meeting the conditions prescribed under NPS

2. Tier 2 Account : This is a voluntary savings account wherein the Subscriber can invest at a low cost, with an aim to provide liquidity. The Subscriber is free to withdraw the savings from this account whenever they wish.

Note: To Open Tier 2 Account Subscriber should have Tier 1 Account if Tier 1 Account is Closed then Tier 2 will be automatically Closed

Investment Choices:

1. Active Choice : If you want complete control of your investments, this is a perfect choice for you. Here you can decide the distribution of your money basis on your Expectations.

There are 4 types of Asset Class in NPS

Asset Class E (Equity) :- Investments in Equity Market (High Risk:High Return)

Asset Class C (Corporate Bonds) :-Investment in Fixed Income Instruments (Moderate Risk : Moderate Return )

Asset Class G (Government Securities):Investment in Government Securities . (Low Risk:Low Return)

Asset Class A (Alternate Assets ):Investments in instruments like CMBS, MBS, REITS, AIFs, etc. ( Very High Risk : Very High Return )

Note : While you have the freedom to decide your investments under NPS, there are certain boundary conditions. These are as below:

• You can invest a maximum of 75% of your pension wealth in equity (Asset class E).

• You can invest a maximum of 5% of your pension wealth in Alternate assets (Asset class A).

• You can invest your entire pension wealth in C or G asset classes.

• You have the option to change your investment choice twice a year.

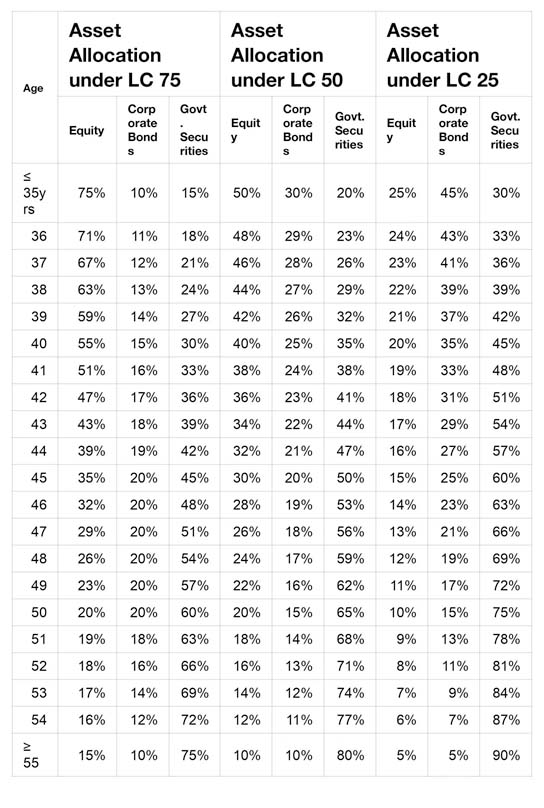

2. Auto Choice : In this Choice NPS gives you option to choose the 3 life cycle options

• LC 75 ( Agressive )

• LC 50 ( Moderate )

• LC 25 (Conservative)

Based on the Option the money is invested in various Asset classes

The Distribution of Money is mentioned Below

Note :

1. Reallocation among the asset classes shall take place on your date of birth every year

2. You may change your preference only twice, at any time during the financial year.

Options Availability after attain Age 60

There are three options available for subscribers once they reach the age of 60 years.

1. Continuation of NPS account:

The subscriber can continue to contribute to NPS account beyond the age of 60 years/superannuation (Up to 70 years). This contribution beyond 60 is also eligible for exclusive tax benefits under NPS.

2. Deferment (Annuity as well as Lump sum amount):

The subscriber can defer Withdrawal and stay invested in NPS up to 70 years of age. The subscriber can defer only lump-sum Withdrawal, defer the only Annuity or defer both lump sum as well as Annuity.

3. Start your Pension:

If the Subscriber does not wish to continue/defer NPS account, he/she can exit from NPS. He/she can initiate exit requests online and asper NPS exit guidelines start receiving a pension.